Third Quarter 2025 Review

Third Quarter 2025 Review

The third quarter was favorable to asset prices with both stocks and bonds providing positive returns for the quarter. The Fed cut interest rates in September for the first time since December of last year, as inflation remained moderately sticky despite tariff policy enacted by the Trump administration. Intermediate interest rates declined slightly throughout the quarter, giving a boost to bond prices. Stocks continue to perform well, backed for the most part by strong corporate earnings. Capital investment in artificial intelligence is surging with the largest tech companies projecting to spend hundreds of billions of dollars as they compete to develop the smartest and newest technologies. Developed and emerging market stocks have continued their 2025 positive performance trend and are still outpacing U.S. equities through nine months.

U.S. Equity Markets

U.S. stocks ticked higher for the quarter as the market applauded the Federal Reserve’s decision to lower interest rates in September. Typically, interest rate cuts provide a tailwind to stocks, which proved the case with the S&P 500 advancing by 8.12% for the quarter. The S&P Mid-Cap 400 Index returned 5.55%. Small cap stocks performed quite well for the quarter by recovering from a rough start to the year. The Russell 2000 Index (small cap index) advanced 12.39% for the quarter. (Smaller companies tend to have higher debt loads, making them more interest rate sensitive.) The September rate cut and expected future rate cuts can make their cost of capital cheaper, allowing them to be more profitable.

Tech stocks also performed quite well for the quarter with the NASDAQ advancing 11.07%, which was fueled by AI. An interesting note from JP Morgan’s Michael Cembalest, stated that “AI related stocks have accounted for 75% of the S&P returns, 80% of earnings growth and 90% of capital spending growth since ChatGPT launched in November of 2022.” Advancements in AI have directly impacted the stock market and the companies benefiting from these technological advances.

Global Markets

International stocks continued to perform well for the third quarter with the EAFE Index, which is an index comprised of developed market stocks, advancing 4.77%. Emerging market stocks also shot up 10.64 %. Over of the last 15 years, U.S. stocks have outpaced international equities, however, for 2025, international stock indexes have performed better. This outperformance is attributed to the combination of the U.S. Dollar’s decline year-to-date and an improving market backdrop in Europe and greater part of Asia. Like the U.S., Europe dealt with surging inflation in 2022, however, inflation has cooled to a year-over-year rate of just 2%, allowing the European Central Bank to cut rates 8 times from a rate of 4% down to 2%. As one can surmise, this process is quite like the U.S., however, unfortunately in our country domestic inflation remains elevated and still above the Fed’s targeted 2% rate.

Fixed Income

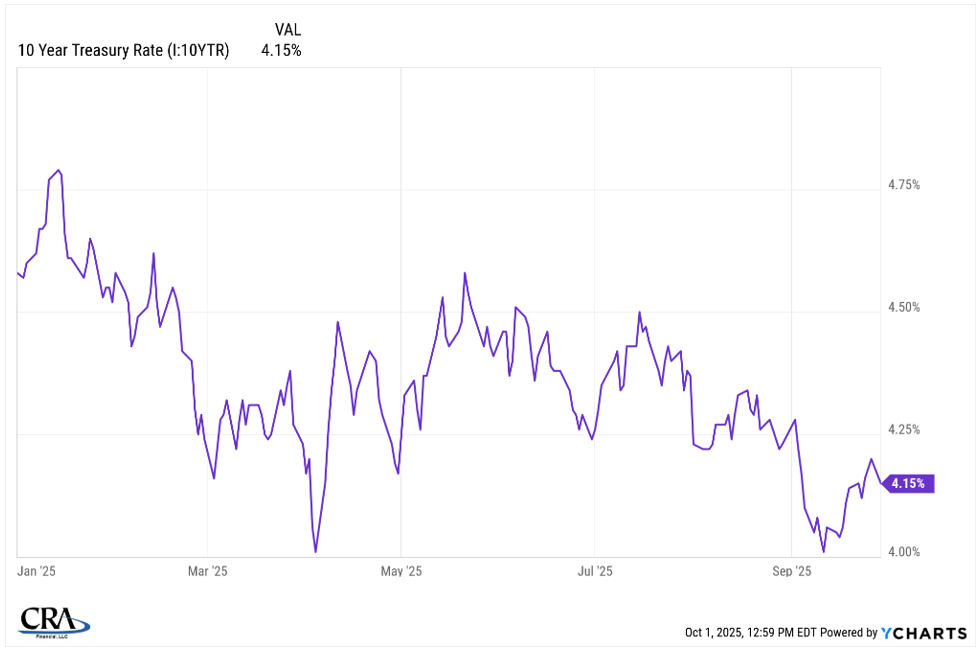

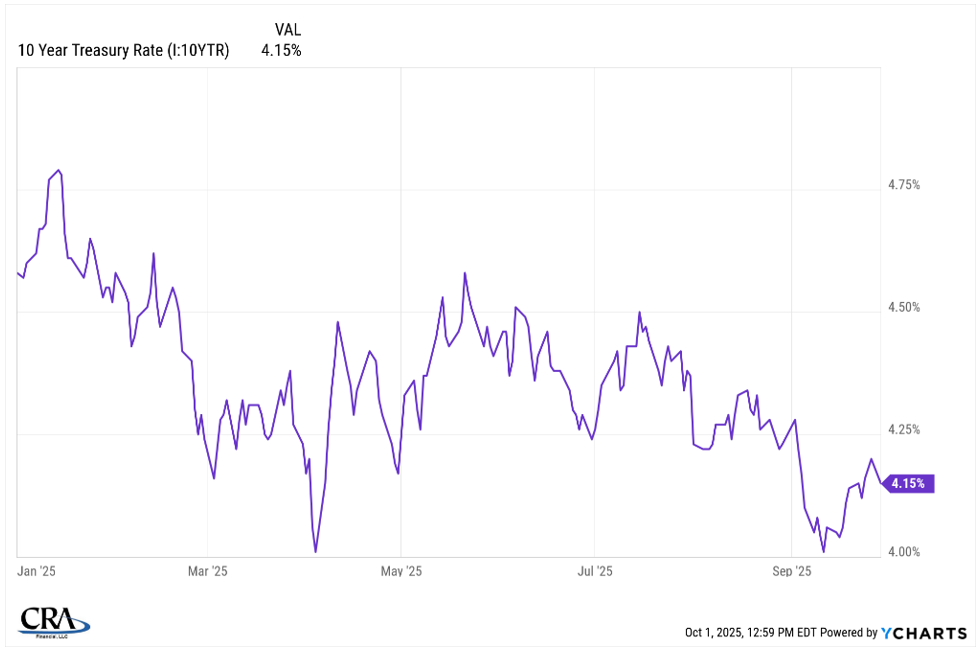

Bonds continued performing well this quarter, with the Aggregate Bond Index advancing 2.03%. Tax-Free Municipal bonds performed better, returning 3%. The Muni bond market performance was lackluster to start the year, so it was nice to see investors rewarded with a bounce back. Longer-term interest rates, like the 10-year treasury yield, declined slightly, which gave a boost to bond pricing. The 10-year and 30-year treasury yields closed the quarter at 4.15% and 4.78% respectively. In our portfolios, we are noticing fixed income beginning to handily outperform cash.

The Federal Reserve

The Fed cut interest rates by .25% in September to a range of 4.00% - 4.25%. The market is expecting 70% chance of 2 more rate cuts for the year. As discussed earlier, this tends to be bullish for stock prices. If inflation data comes in hotter than expected, this could lower the likelihood of this occurring which could cause the market to sell off. Still, the trendline for interest rates appears to be heading lower, which can help boost the economy as well as the stock market. The Fed’s moves as well as their commentary will dictate much of the market moves in the months ahead to close out the year.

U.S. Dollar Takes an Historic Dip

In the first half of 2025, the U.S. dollar saw its worst performance in over 50 years, plunging more than 10% based on the U.S. Dollar Index. For the third quarter, the Dollar stabilized and advanced just north of 1%. A declining U.S. Dollar is not necessarily something to panic over as it does make U.S. exports cheaper which can help reduce the trade deficit.

Cryptocurrencies

In the third quarter, the cryptocurrency market showed mixed but generally positive performance, with Ethereum notably outperforming Bitcoin. While Bitcoin posted modest gains amid low volatility and continued institutional ETF inflows, Ethereum surged benefiting from increased network activity and renewed interest in smart contract platforms. Altcoins across sectors like DeFi, AI, and consumer tokens also saw strong returns, driven by capital rotation and growing demand for utility-based assets. However, on-chain metrics such as transaction fees and user activity declined quarter-over-quarter, raising concerns about the sustainability of the rally. Despite strong price action, the market's low volatility and weakening fundamentals suggest caution heading into the fourth quarter.

Energy & Commodities

Oil prices ended the quarter at $62.37, quietly down 10% from just a year ago. Gold ended the quarter at $3,840.80 per ounce, up over 40% on a year over year basis.

2025 Final Look

U.S. stocks have remained resilient for the year, looking past the volatility that occurred following the “liberation day” tariff policy. Many of our clients seem somewhat in disbelief of the market, but stocks tend to “climb a wall of worry” as is often said on Wall Street. The quick rebound from a dip and subsequent rise to all-time highs feels somewhat like the rebound that stocks exhibited coming out of the 2020 global pandemic. Many clients then felt uneasy about geopolitics or the world outlook in general, yet the market churned higher. The economy remains on solid footing with a Fed that is now easing on their monetary policy which could be supportive of stocks moving higher to close out the year. Still, stock valuations could be somewhat stretched when comparing historical price to earnings ratios compared to where we stand today. As your advisors, we look forward to helping you navigate and connect the dots as we plan for 2026 and beyond.

As always, let us know if you have any questions.

Best,

CRA Investment Committee

Matt Reynolds CPA, CFP®

Tom Reynolds, CPA

Robert T. Martin, CFA, CFP®

Gordon Shearer Jr., CFP®

Jeff Hilliard, CFP®, CRPC®

Joe McCaffrey, CFP®

Phillip Tompkins, CFP®

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CRA Financial, LLC [“CRA]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CRA. Please remember to contact CRA, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CRA is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of CRA’s current written Disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.crafinancial.com. Please Note: If you are a CRA client, please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your CRA account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your CRA accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if CRA is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (to the extent applicable). Unless expressly indicated to the contrary, CRA did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of CRA by any of its clients. ANY QUESTIONS: CRA’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.