First Half of 2025 Review

First Half of 2025 Review

The first half of the year had no shortage of drama with the market experiencing an intraday low on April 8th that was about 20% lower than the all-time high reached in mid-February. A sharp dip occurred after President Trump’s “Liberation Day” announcement on April 2nd, where proposed tariffs from the administration came in considerably higher than what the market was prepared for. President Trump delayed some tariffs and in the subsequent weeks, the market recovered and even made an all-time high by the close of Q2 on June 30th. The chart of the S&P 500 (see below) shows a quick “V”-shaped recovery reminiscent of 2020 when we saw a plunge from the global pandemic followed by a snap-back in asset prices.

This was just part of the story for the first half of the year. Geopolitics also took center stage with the U.S. becoming directly involved in the conflict within the Middle East, ultimately striking nuclear facilities in Iran. Additionally, a Republican majority Congress pushed to meet President Trump’s self-imposed July 4th deadline for the Big Beautiful Bill, which primarily centered on the 2017 tax cut extension, further tax relief, and additional border security. It was in fact signed into law by President Trump on Independence Day.

U.S. Equity Markets

Stocks initially climbed nearly 5% before dropping roughly 20% on April 8th. A drop of over 10% is typically referred to as a “correction” for the stock market. While U.S. stocks ended lower for the first quarter, the U.S. Broad Market Index returned nearly 11% in the second quarter. Year-to-date, the S&P 500 has returned 6.2%, rewarding investors who maintained their stock portfolio throughout this volatile period. The Dow Jones has advanced a bit less, up 4.55% and the tech-heavy NASDAQ is up 5.85% for the first half of 2025.

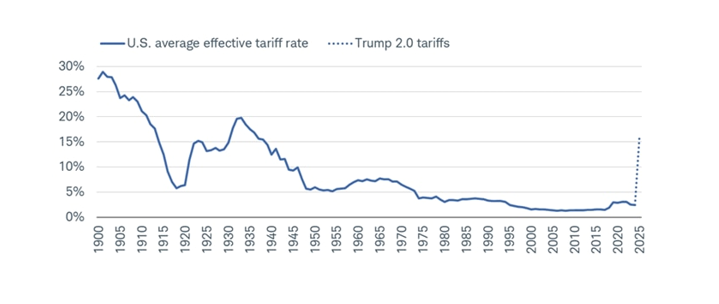

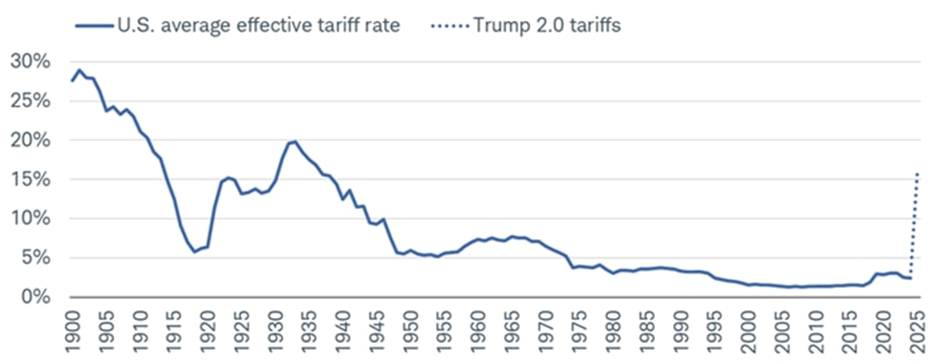

Tariffs remain a significant risk to the stock market, with uncertainty about their economic impact. The Fed was cutting rates last year and stopped in 2025 as they have stated that they do not know how tariffs will impact inflation. The fear is that these tariffs could reignite higher prices. This would be terrible news for the U.S. economy, which is already financially stretched with a federal debt load that has surged over recent years. It is also possible that the President will continue pushing back tariffs and provide enough exceptions that inflation will not be impacted. President Trump has extended his July 9th extension date out to August 1st with a warning to negotiate in good faith by then or face the originally announced April 2nd tariffs again.

Global Markets

A bright spot was seen in international stocks throughout the first half of the year. The EAFE Index, which is an index comprised of developed market stocks, advanced 19.45%. Emerging market stocks also shot up 15.27% with Chinese stocks moving higher.

While it was great to see international stocks advance, as noted in the prior quarterly write-up, international stocks have performed poorly when taking a long-term perspective into account. As of the end of 2024, the S&P 500 performed around three times better than the international index over a five-year period. It is possible that these stocks were priced too low, and that international stocks have some room to continue to move higher; however, our firm reiterates an underweight to international stocks in relation to U.S. equities. We expect the U.S. in the long-term to continue to outperform most other markets given a long trendline of outperformance. Additionally, a good portion of the returns from international stocks thus far in 2025 are attributable to the U.S. dollar’s large first-half decline.

Fixed Income

Bonds rallied in the first half of the year, with the Aggregate Bond Index advancing 4.02%. Some of this return is attributed to a recovery from the 4th quarter of 2024 in which bonds lost around 3%. Interest rates continue to be quite volatile as bond market investors try to pinpoint the Federal Reserve’s path forward. Nonetheless, this gain for bonds is the result of longer-term interest rates declining, as evidenced by the 10-year Treasury, which started the year at 4.56% but ended the second quarter yielding just 4.23%.

Falling interest rates during the recent stock market downturn provided welcome relief for diversified investors. Advisors often pair stocks and bonds in portfolios to create balance, as these assets can behave differently in various market conditions. Typically, when stocks decline, interest rates also fall—boosting bond prices. This dynamic, which played out again this year, helps stabilize portfolios by ensuring that bonds deliver returns even when equities are under pressure.

The Fed

The Federal Open Market Committee (FOMC) met four times, January, March, May, and June, and consistently maintained the benchmark federal funds rate at 4.25 %–4.50%, citing a robust labor market and persistent inflation pressures. During June's meeting, Fed Chair Jerome Powell reinforced a “no rush to cut rates” stance, despite growing market expectations. However, the updated Dot Plot projections in June signaled a shift, indicating two rate cuts likely by year-end, with inflation projected to remain above target (around 3%) and unemployment gradually rising.

Fed commentary remained cautious: Atlanta Fed’s Raphael Bostic affirmed there was no urgency given the strong labor markets and tariff worries, though he expected one cut in 2025. Meanwhile, other policymakers like Waller, Bowman, and Daly expressed openness to a possible July cut if data warranted. Goldman Sachs upgraded its forecast to three cuts (Sept, Oct, Dec) in 2025, reflecting lighter tariff inflation and signs of labor weakening. Overall, markets have priced in a September rate cut, but the Fed is sticking to a cautious, data-dependent approach, balancing the trade‑off between cooling inflation and avoiding premature easing.

U.S. Dollar Takes a Historic Dip

In the first half of 2025, the U.S. dollar saw its worst performance in over 50 years, plunging more than 10% based on the U.S. Dollar Index. Trade wars, sticky inflation, and rising government debt led to this decline. The dollar was also quite strong toward the end of 2024, so it certainly had room to retreat.

As noted earlier, a weakening dollar leads to higher returns for international stocks. It also makes it more expensive for Americans to travel or to import goods from overseas. The positive is that a weaker dollar makes U.S. goods cheaper for foreigners and this weakened currency can help to balance the trade deficit. The chart on the left shows that, despite this recent decline, the dollar remains within a normal historical range.

Cryptocurrencies

In the first half of 2025, the cryptocurrency market delivered a mixed and relatively subdued performance. Bitcoin posted modest gains of around +13% year-to-date, supported by continued interest in spot ETFs and deregulation of the Trump administration, though the rally lost steam amid broader risk-off sentiment in financial markets. Ethereum underperformed, slipping into negative territory as enthusiasm waned due to delays in protocol upgrades and weaker demand for DeFi and NFT activity. While institutional interest remained steady, overall crypto trading volumes were lower than in previous bull cycles, and altcoins showed choppy, uneven performance. The first half of 2025 reflected a period of consolidation, with investors waiting for clearer macroeconomic signals and technological developments.

2025 Outlook

The S&P 500 is up 24.5% since hitting its low point on April 8th. It should be expected that things would slow down in the subsequent quarters to end this year. There is no shortage of risk and uncertainty which the stock market isn’t fond of. The stock market tends to perform the best when the President has limited power with Congress controlled by the other party. The changing rules surrounding tariffs, taxes, and interest rates should lead to continued volatility as we progress through the year. Still, as seen recently, volatility works both ways. At times the market shoots higher when investors perceive an outcome as good news. If the first half has proven anything, remaining disciplined and not abandoning your investment strategy is a winning formula for long-term success.

As always, let us know if you have any questions.

Best,

CRA Investment Committee

Matt Reynolds CPA, CFP®

Tom Reynolds, CPA

Robert T. Martin, CFA, CFP®

Gordon Shearer Jr., CFP®

Jeff Hilliard, CFP®, CRPC®

Joe McCaffrey, CFP®

Phillip Tompkins, CFP®

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by CRA Financial, LLC [“CRA]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from CRA. Please remember to contact CRA, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. CRA is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of CRA’s current written Disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.crafinancial.com. Please Note: If you are a CRA client, please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your CRA account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your CRA accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if CRA is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (to the extent applicable). Unless expressly indicated to the contrary, CRA did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of CRA by any of its clients. ANY QUESTIONS: CRA’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.